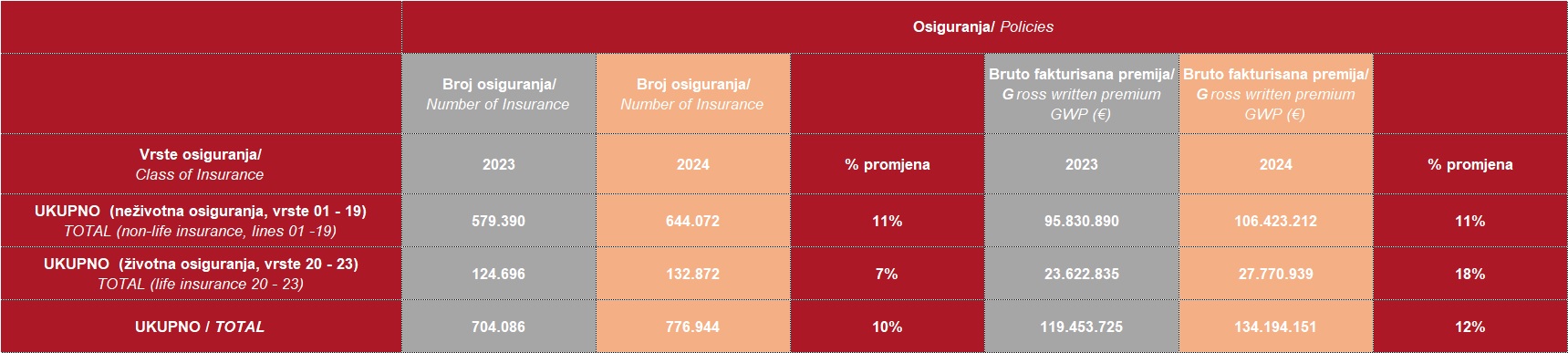

- The TOTAL NUMBER OF INSURANCE POLICIES in 2024 increased by 10.3 percent compared to 2023, from 704,086 in 2023 to 776,944 in 2024.

- 47 percent of the total number of policies in the non-life insurance segment are motor vehicle liability insurance policies.

- GROSS WRITTEN PREMIUMS at the end of 2024 were 12.3 percent higher than the previous year, from €119.5 million to €134.2 million.

- The NUMBER OF REPORTED CLAIMS in 2024 increased by 19 percent, from 80,500 to 95,763.

- The AMOUNT OF SETTLED CLAIMS increased from €49.8 million in 2023 to €60 million in 2024.

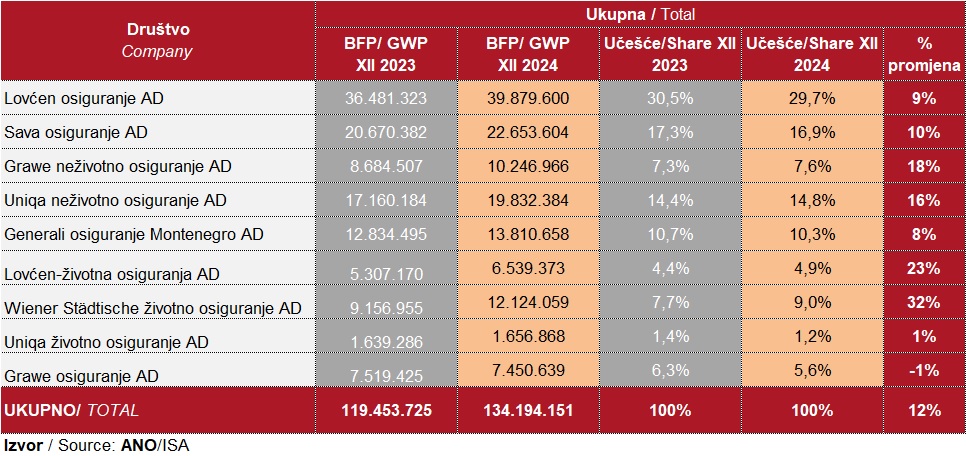

- Lovćen osiguranje AD continues to dominate the market with the largest share of 29.7 percent of the total gross premium.

- Wiener Städtische životno osiguranje AD achieved the highest annual premium growth of 32 percent.

- BUSINESS REVENUES of insurance companies show a general trend of growth, with an increase of about 8 percent compared to 2023 at the sector level.

- TOTAL ASSETS of insurance companies show a generally stable trend of growth, with an increase at the sector level of about 9 percent compared to 2023.

- LONG-TERM FINANCIAL INVESTMENTS show a trend of decline at the end of 2024 compared to the previous year, by 14 percent.

- SHORT-TERM FINANCIAL INVESTMENTS show a trend of growth: 2023: €23.7 million, 2024: €80.4 million.

- FINANCIAL RESULTS FROM INVESTMENTS show an extremely positive trend, with a total increase of about 24 percent at the sector level compared to the previous year.

- NET PROFIT of insurance companies shows mixed results, with a total increase of about 3 percent compared to 2023 at the sector level.

- INSURANCE PENETRATION (ratio of insurance premiums to GDP) in OECD countries for NON-LIFE INSURANCE was about 2.5 percent of GDP, in Croatia 2.1 percent, in Slovenia 3.2 percent, and in Montenegro 1.7 percent.

- INSURANCE PENETRATION (ratio of insurance premiums to GDP) in OECD countries for LIFE INSURANCE was about 3.5 percent of GDP, in Croatia 1.5 percent, in Slovenia 2 percent, and in Montenegro 0.35 percent.

The Insurance Supervision Agency recently published financial reports of insurance companies operating in Montenegro on its website, which showed different results in key financial indicators for the year behind us. Some companies recorded significant growth, some stagnated, while others faced reduced income and profits.

However, before we delve into the details of the business of insurance companies during 2024, we want to briefly review the analysis of the local insurance market at an aggregate level. During the previous year, we could see that the insurance market was experiencing significant changes, both in terms of the number of policies issued and the amount of gross written premiums, as well as the number and amount of reported (and settled) claims. According to data from regular monthly reports on the state of the sector available on the Insurance Supervision Agency’s website, it can be observed that different types of insurance developed differently, with some types recording impressive growth, while others showed stagnation or even decline.

The total number of insurance policies in 2024 increased by 10.3 percent, from 704,086 in 2023 to 776,944 in 2024. This growth is a result of an increase in the number of policies both in non-life and life insurance segments. Specifically, the number of non-life insurance policies increased by 11 percent, while life insurance policies increased by 7 percent. When it comes to the number of issued insurance policies by type, motor vehicle liability insurance policies have the largest share, with 304,926 policies issued in 2024, representing a growth of 7.2 percent compared to the previous year. This type of insurance accounts for 47 percent of the total number of policies in the non-life insurance segment. A significant increase was also recorded in travel insurance, where the number of policies rose from 93,749 to 108,577, representing an impressive growth of 15.8 percent on an annual basis.

A similar trend can be observed in terms of gross written premiums, where the total amount increased from €119.5 million in 2023 to €134.2 million in 2024, representing an annual growth of 12.3 percent. However, the structure of growth was different, with non-life insurance premiums growing by 11 percent and life insurance premiums increasing by 18 percent on an annual basis.

In terms of specific categories, motor vehicle liability insurance again dominates with an amount of €47 million in 2024, representing a growth of 9 percent compared to the previous year. This type of insurance accounts for 45 percent of the total premium amount in the non-life insurance segment. A significant increase was also recorded in life insurance, where premiums rose from €21.7 million to €25.4 million, representing an annual growth of 17 percent. On the other hand, marine insurance recorded a decline in premiums from €564,000 to €324,000, which is an annual decrease of 42.6 percent. Interestingly, during 2024, there was also a decrease in the amount for credit insurance by 12 percent, although the number of policies issued in this segment increased by 10 percent on an annual basis.

The number of reported claims in 2024 increased by 19 percent, from 80,500 to 95,763. The largest number of claims was recorded in the health insurance segment, where the number of claims increased from 36,645 to 46,195, representing a growth of 26 percent. The amount of settled claims also increased, from €49.8 million in 2023 to €60 million in 2024. The largest amount of settled claims was recorded in motor vehicle liability insurance, where it increased from €18.5 million to €23.4 million, representing an annual growth of 26.4 percent.

From the same reports, we can see how the gross written premium for the past two years changed among individual companies, as well as the differences in market share among them. Lovćen Osiguranje AD continues to dominate the market with the largest share, although its share slightly decreased from 30.5 percent in 2023 to 29.7 percent in 2024. This company recorded an annual growth in gross premium of 9 percent. Sava Osiguranje AD, the second-largest, also reduced its share from 17.3 percent to 16.9 percent, with a growth in gross written premium of 10 percent.

The company with the largest absolute change in gross written premium was Wiener Städtische životno osiguranje AD, with an annual growth of 32 percent. This company significantly increased its market share from 7.7 percent to 9 percent, which is the largest relative growth among all insurance companies. This jump indicates a successful strategy and growing popularity of life insurance.

Grawe neživotno osiguranje AD also showed impressive growth in gross premium of 18 percent, increasing its market share from 7.3 percent to 7.6 percent. Uniqa neživotno osiguranje AD followed with an annual growth in gross written premium of 16 percent, further strengthening its market share from 14.4 percent at the end of 2023 to 14.8 percent at the end of 2024. Meanwhile, Lovćen životno osiguranje AD recorded a premium growth of 23 percent, which is the second-largest relative growth in the market.

On the other hand, Grawe osiguranje AD (life) was the only company that recorded a decline in gross written premium, with a decrease of 1 percent, while Uniqa životno osiguranje AD had a minimal annual premium growth of just 1 percent.

These data indicate that while traditional leaders like Lovćen and Sava continue to hold the largest shares in the market, dynamic changes and growth among other players, especially in the life insurance segment, could lead to further changes in the market.

Overall, the insurance market in Montenegro shows signs of healthy growth, and how this growth in gross premium affected the financial operations of companies will be discussed further.

ANALYSIS OF BUSINESS

The business of insurance companies in Montenegro shows positive trends in 2024, with significant changes in revenues, financial results, and total assets. An analysis of the data from the business reports of companies for 2024 compared to the previous year reveals how individual companies dealt with market challenges and where they sought opportunities for growth.

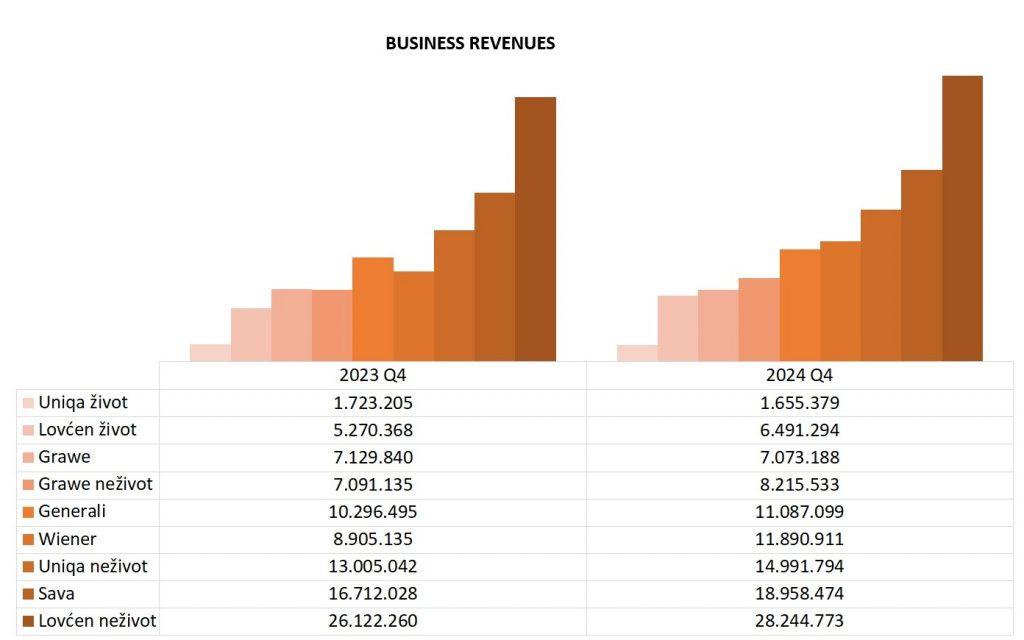

BUSINESS REVENUES of insurance companies show a general trend of growth, with an average increase of about 8 percent compared to 2023.

Lovćen osiguranje AD achieved the highest revenue of €28.2 million in 2024, representing a growth of 8 percent compared to 2023. Sava osiguranje AD also recorded a similar growth trend, with revenue of nearly €19 million, which is 13 percent higher than the previous year. Uniqa neživotno osiguranje AD also reported a revenue increase of 15 percent, while Generali osiguranje Montenegro AD had a more modest growth of 7.7 percent.

The largest absolute growth during the previous year was achieved by Životno Wiener osiguranje, which recorded almost €3 million more in revenue during 2024 than the year before.

However, some companies recorded a decline in revenue. Grawe osigiranje AD had a slight decrease of 0.8 percent, while Uniqa životno osiguranje recorded a decline of 3.9 percent. These data indicate different strategies and market conditions that affected the performance of individual companies.

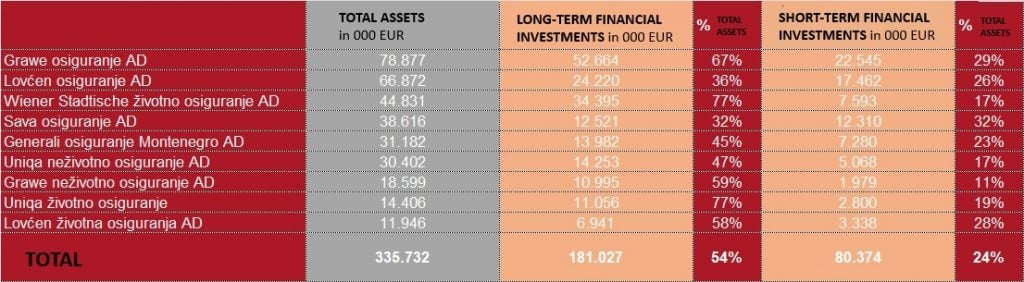

TOTAL ASSETS of insurance companies show a generally stable trend of growth, with an increase at the sector level of about 9 percent compared to 2023. Grawe osiguranje AD had the largest total assets in the amount of €78.9 million, representing a growth of 5.1 percent compared to 2023. Wiener Stadtische životno osiguranje AD recorded the largest percentage annual growth of 21.4 percent, with assets valued at €44.8 million.

Lovćen osiguranje‘s assets also showed significant growth of 10.6 percent, while all other companies increased their total assets, indicating stability and growth in the insurance sector in Montenegro.

Most of their assets are invested in financial investments, which generate interest income that largely affects the final business result. A review of the asset structure of insurance companies will be provided in the table:

The majority of these investments are defined through accounts of long-term or short-term investments, primarily referring to securities, which we detailed last year when analyzing the business results for the first nine months of the previous year. At that time, we presented in detail how companies allocate their funds, into which types of securities, from which countries they are issued, what maturity period they have, etc.

It is interesting to note that LONG-TERM FINANCIAL INVESTMENTS show a trend of decline at the end of 2024 compared to the previous year, by 14 percent (2023: €209.6 million, 2024: €181 million), while on the other hand, SHORT-TERM FINANCIAL INVESTMENTS grew significantly during the previous year by 240 percent (2023: €23.7 million, 2024: €80.4 million). This indicates changes in investment strategy. The reason for this lies either in accounting policies that change the maturity period of certain securities or in the fact that during the previous year, interest rates on short-term debt securities issued by European Union countries maintained a high level, which likely attracted companies to invest in this type of asset.

Grawe osiguranje AD had the largest long-term investments amounting to €52.7 million, which represented two-thirds of the company’s total assets, with a year-on-year decrease in investments of this type by 25 percent. At the end of 2023, this company held €680,000 in short-term investments, which increased to €22.5 million by the end of 2024.

Generali osiguranje Montenegro AD also recorded a 25 percent decrease in long-term investments, while simultaneously increasing short-term investments by 510 percent on an annual basis.

On the other hand, Wiener Stadtische životno Osiguranje AD recorded a 3.6 percent increase in long-term investments, indicating a continued strategy of investing in long-term projects, which is more typical of life insurance companies than those offering non-life insurance services.

Sava Osiguranje is a company that maintains almost identical levels of assets in both long-term and short-term investments (each around €12 million), although it also adjusted its investment portfolio during the previous year in favor of short-term investments.

All these investments have enabled companies to achieve FINANCIAL RESULTS FROM INVESTMENTS that show an extremely positive trend, with a total increase of about 24 percent at the sector level compared to the previous year. This growth can be attributed to favorable market conditions, successful investments in financial instruments, and portfolio diversification. Grawe osiguranje AD achieved the highest financial result from investments in the amount of €2.8 million, which is 3.9 percent more than in 2023. Wiener Stadtische životno Osiguranje AD recorded a significant increase of 35.4 percent with a result of €1.8 million, while Lovćen osiguranje AD also showed an impressive growth of 47.1 percent, indicating a successful investment strategy.

Uniqa neživotno osiguranje AD recorded the largest growth in this category, with an 81 percent better result compared to the previous year, and all these data indicate that insurance companies have managed to achieve positive results through efficient management of their investments.

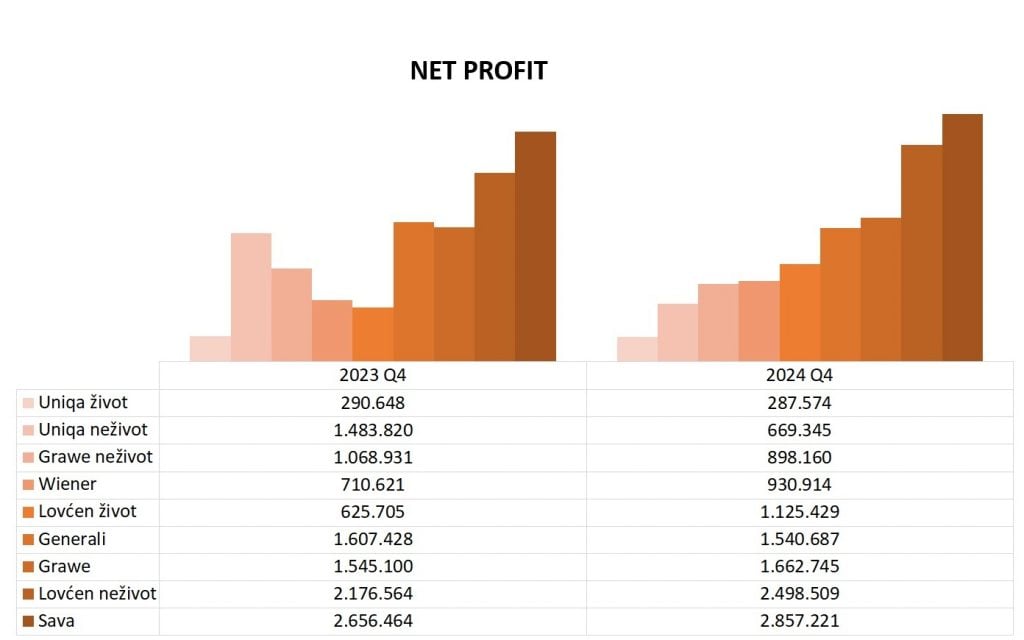

The NET PROFIT of insurance companies shows mixed results, with a total increase of about 3 percent compared to 2023 at the sector level. Sava osiguranje AD achieved the highest net profit in the amount of €2.8 million, representing a better result of 7.5 percent compared to 2023. Lovćen osiguranje AD also recorded an annual profit growth of 14.8 percent, with a net profit of €2.5 million. Wiener Stadtische životno osiguranje AD achieved a net profit growth of 31 percent, indicating successful operations and good financial results.

However, some companies faced a decrease in net earnings compared to the previous year. Grawe neživotno osiguranje AD recorded a net earnings decrease of €170,000, Uniqa neživotno osiguranje AD achieved a net profit of only €669,000 during the previous year, while Generali osiguranje Montenegro AD recorded a profit decline of 4.1 percent.

GLOBAL TRENDS AND MONTENEGRO

Now that we have seen how vibrant the local insurance market is, it is time to focus on GLOBAL TRENDS IN COMPARISON TO LOCAL CONDITIONS where possible. To this end, we provide insights from the annual report Global Insurance Market Trends 2024, recently published by the Organization for Economic Co-operation and Development (OECD), an international institution founded in 1961 to promote economic development and world trade, headquartered in Paris. Their latest report explores the state and trends in the global insurance sector during 2023, focusing on premium growth, claims payments, investment performance, and the profitability of insurance companies, covering over 50 countries, including OECD members and some non-OECD countries.

Non-life insurance continues to dominate the global market, accounting for 55 percent of total gross written premiums. Motor vehicle insurance has the largest share in this sector, making up more than a third of premiums on average, while in some countries, motor vehicle insurance accounts for over 50 percent of premiums in the non-life sector. Health insurance is also a significant class in the non-life sector, with an average share of 23 percent in total premiums. In countries like the Netherlands, the USA, and Switzerland, where private health insurance is the primary mechanism for health protection, this share is significantly higher.

The average INSURANCE PENETRATION (ratio of insurance premiums to GDP) in OECD countries varies but is generally higher in developed economies. In 2023, the average penetration for non-life insurance was about 2.5 percent of GDP, while for life insurance it was about 3.5 percent of GDP. In some countries, such as France, the UK, and the USA, insurance penetration exceeds 10 percent of GDP. On the other hand, the lowest insurance penetration is recorded in many Latin American countries, such as Bolivia, Nicaragua, and Guatemala, where premiums make up a smaller part of GDP.

For comparison, in Croatia, insurance penetration is lower than the OECD average: non-life insurance premiums account for about 2.1 percent of GDP, while life insurance premiums account for about 1.5 percent of GDP. Slovenia has a slightly higher insurance penetration compared to Croatia, with non-life insurance premiums at around 3.2 percent of GDP and life insurance premiums at around 2.0 percent of GDP. In 2023, the share of premiums in Montenegro‘s GDP (insurance penetration) was 1.74 percent, and despite the growth of total premiums in the market, it recorded a decline compared to 2022 due to a significant increase in Montenegro’s GDP in 2023. The penetration of non-life insurance was 1.40 percent, while the penetration of life insurance was 0.35 percent.

Another indicator used to analyze the development of the insurance market is INSURANCE DENSITY, which represents the amount of insurance premiums per capita of a given country. If we compare the amounts of gross written premiums by insurance type relative to the population, we see that the amounts allocated for insurance purposes are increasing year by year. Thus, the average allocation for non-life insurance at the end of 2024 was €170.7, which is 13 percent more than the previous year, while for life insurance, an average of €44.5 was allocated, representing an increase of 19 percent compared to 2023.

However, these figures are far from the average that citizens of developed European countries allocate for these purposes. According to data from the EIOPA report (European Insurance and Occupational Pensions Authority) for 2023, we can see that average allocations for life insurance range from €70 per year in Croatia, €167 in Slovenia, €831 in Italy, €847 in Germany, €2,235 in France, to the remarkably high €5,630 in Ireland, €7,508 in Luxembourg, and €9,247 in Liechtenstein.

In 2023, the AVERAGE PREMIUM GROWTH in OECD countries was 12.4 percent in nominal terms for non-life insurance, which is lower compared to the growth in 2022 (14.1 percent). The largest premium growth was recorded in Turkey (premium growth in the non-life insurance sector was 112.1 percent in nominal terms, while in the life insurance sector it was 83.4 percent) and Argentina (premium growth for motor vehicle insurance was 117.6 percent, while for property insurance against fire and other damages it was 108.1 percent).

If we again look at the analyzed countries in the region, we see that in the non-life insurance sector, Croatia recorded a premium growth of 21.7 percent for motor vehicle insurance and 10.1 percent for health insurance, while in Slovenia, the premium growth for motor vehicle insurance was 20 percent.

When it comes to CLAIMS in the non-life insurance sector at the OECD level, they continued to rise in 2023, with an average nominal growth of 17 percent. This growth is due to increased repair costs, medical expenses, and the frequency of disasters. According to Swiss Re, total insured losses from natural disasters were $108 billion, which is less than in 2022, but the frequency and intensity of these events remained high. Turkey recorded significant losses due to the earthquakes in February 2023, which affected the growth of premiums that local residents and businesses began to allocate after the disaster. Regarding the region, claims in Croatia‘s non-life insurance sector increased by 14.3 percent in 2023, while in Slovenia, they increased by 13.7 percent.

Finally, it is important to note that INSURANCE PRICES have risen in most OECD countries, especially in the sectors of motor vehicle insurance, health insurance, and property insurance. The average price increase for motor vehicle insurance was 12.5 percent, while for health insurance it was 8.8 percent, and for property insurance, the average price increase was 9.2 percent. In the future, key challenges for the industry will be managing risks related to climate changes and adapting to new regulatory standards, which will have a significant impact on the presentation of financial results of insurance companies.

CONCLUSION

The previous analysis showed that insurance companies in Montenegro achieved good results during the previous year, with significant growth in certain categories, but also challenges in others. Lovćen Insurance AD and Sava Insurance AD stood out as leaders in revenues and net profits, while financial results from investments show positive trends, indicating successful investment management. Total assets and gross written premiums also show growth, indicating stability and growth in the insurance sector in Montenegro. However, changes in long-term financial investments in favor of short-term investments suggest an adaptation of strategies in line with market conditions, for which it is questionable how sustainable they are in the long term. Overall, most companies managed to achieve positive results in all segments of their operations, indicating stability and strengthening of the sector.